If you own a business, you are required to report personal property that is used in your business to your appraisal district.

A rendition is a form that provides the appraisal district with taxable business property information. This form includes the business name and location, a description of assets, cost and acquisition dates, and an opinion of value for business personal property. The appraisal district uses the information to estimate the market value of your business property for annual property tax purposes. Texas requires a business to pay property taxes to each taxing unit based on the market value of the inventory and assets it owns or uses in the production of income.

To File

The deadline to file a rendition is April 15.

Renditions may be mailed to the address below or delivered to our office location:

Mailing Address: 900 S. Seguin Avenue, New Braunfels, TX 78130

If you would like to file a rendition online, you may submit the form online using our online portal. You will be prompted to create a new login by using an email address and password. The Online Forms – Status item in the online portal will confirm your rendition has been submitted. Late renditions will not be accepted through the online portal.

CAD cannot confirm receipt of renditions, extension requests, or exemption forms, etc. If you require confirmation, please choose a submission method that will provide delivery confirmation.

For questions, please call (830)625-8597 to speak with a customer service representative or e-mail your question(s) to cadbpp@co.comal.tx.us.

HOW TO COMPLETE A BUSINESS PERSONAL PROPERTY (BPP) RENDITION

The Texas Property Tax Code requires all personal property owned by a business for the purpose of producing an income to be reported, or rendered, to the appraisal district for valuation on an annual basis.

Things to Remember:

The rendition is concerning personal property owned by the business on January 1st of the tax year.

Only tangible personal property such as furniture, fixtures, equipment, inventory, etc. are taxable. Intangibles such as cash, stocks, accounts receivable, and other paper assets are not taxable.

The BPP rendition form is due by April 15th each year. Deadline extensions (30 day extension) are available with a written request before the April 15th.

The rendition forms are not mailed to business owners. They can be found on the appraisal district website www.comalad.org/forms or the State comptroller’s website. If you have a valid email address on your account, you will receive a courtesy reminder to file by email.

The Appraisal District’s name will be Comal Appraisal District if your business personal property is physically located in Comal County.

Renditions do not need to be notarized if the owner is the person filing it out.

All fields are required unless otherwise indicated as ‘optional’.

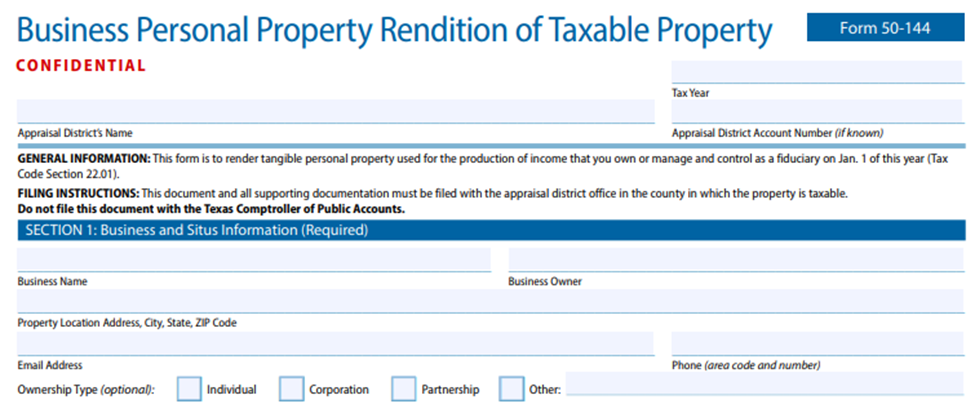

Section 1: Business & Situs Information

Ownership Type is optional, but helpful.

At the very top, you will indicate the tax year for which the rendition applies.

Business Name should be consistent with your Secretary of State filings.

Business Owner should also be consistent with your Secretary of State filings.

Property Location is the actual, physical location of the business personal property assets; also called the situs.

Contact Email and Phone Number should be provided for easy communications.

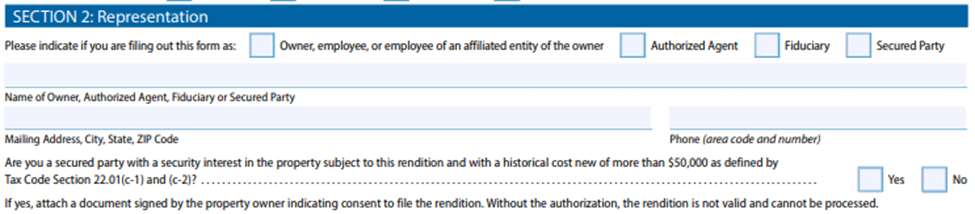

Section 2: Representation

Is this form being completed by the owner? Authorized agent? Fiduciary? Secured Party? Please indicate.

If this form is being filed by the owner, repeat name and phone number.

Provide the mailing address you would like communications to be sent; this does not have to be the same as the property location.

The mailing address indicated will be added to our records & any correspondence regarding your BPP account will be sent there.

Indicate whether you are a secured party with a security interest in the property. If you are not sure what this is, please consult your legal counsel.

Documentation is required if selecting “Yes”.

Section 3: Affirmation of Prior Year Rendition

Was your prior year rendition filing the same as this year?

Your assets must be exactly the same as the previous year (no addition or disposal of assets).

Check the box and add the prior tax year, if applicable.

If section 3 is applicable, no other schedules are required. please complete only Sections 1 through 6 of the rendition.

If your depreciated assets have no changes, but you have updated your inventory/supplies values, you may check this box AND update schedule B or C as applicable.

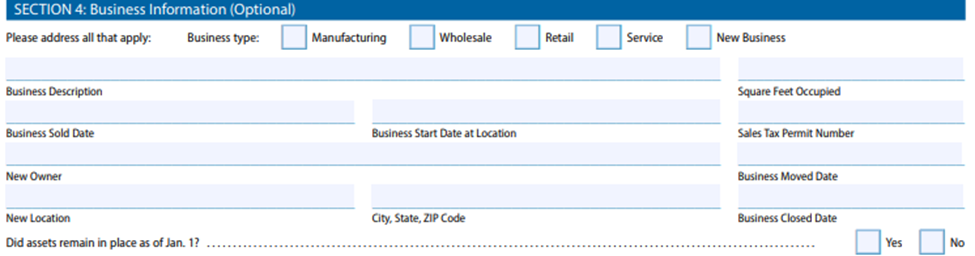

Section 4: Business Information

Did assets remain in place as of Jan 1st? Or were they moved elsewhere?

Section 4 is optional, but the information provided is helpful for our appraisers and should be answered if applicable.

What is your business type? Manufacturing? Wholesale? Retail? Service? New business? Check any that may apply.

Business description will help us to properly classify your property.

If you sold or moved your business, you will indicate so in the appropriate field. Failure to do so may result in erroneous tax statements and lengthy correction processes.

Section 5: Market Value

What is the approximate total market value of your personal property? Under $20,000? Or over $20,000? Check one that applies.

The requirements for filing with property under $20,000 are different than for businesses valued over $20,000.

Under: Complete Schedules A and F, if applicable.

Over: Complete schedules B, C, D, E, and/or F, as applicable.

What is the approximate total market value of your personal property? Under $125,000? Or over $125,000? Check one that applies.

If your value is under $125,000 check the box under as well stating you certify your value is under $125,000.

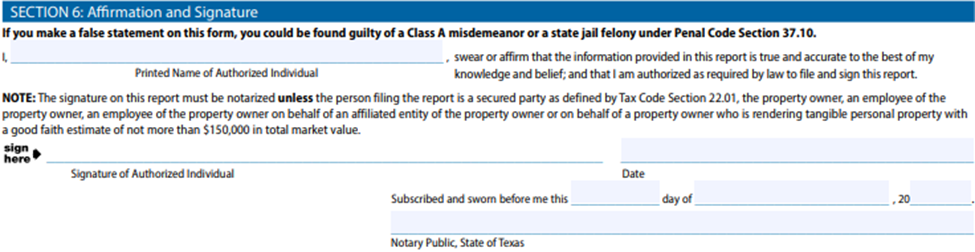

Section 6: Affirmation & Signature

The rendition must be signed by an authorized person to be valid.

Printed Name of Authorized Individual (REQUIRED)– The person who either owns the property, is the agent, or holds fiduciary responsibility for the business & is filing this rendition.

Signature of Authorized Individual (REQUIRED) – should be the same person as the Printed Name of the Authorized Individual.

If the person filing and signing this report is the property owner or an employee of the property owner, they are not required to get this form notarized.

Note: If the person filing and signing this report is not the property owner, an employee of the property owner, an employee of a property owner signing on behalf of an affiliated entity of the property owner, or a secured party as defined by Tax Code Section 22.01, the signature must be notarized.

If the person filing and signing this report is an agent or entity filing on behalf of a property owner who is rendering tangible personal property only with a good faith estimate of more than $150,000 in total market value, the signature must be notarized.

Schedule A: Personal Property Valued Less Than $20,000

The “optional” questions are useful to our appraisers and should be answered if applicable.

This section is applicable to businesses with less than $20,000 in business personal property.

Under Schedule A, list all general property descriptions by type/category. Categories may include furniture, fixtures, machinery, office equipment, computer equipment, signage, inventory, raw materials, supplies, and vehicles.

Note: if you list inventory, supplies, or vehicle assets here under Schedule A, you do not need to add them under Schedules B,C, or D respectively. We do not want to duplicate any assets.

Add an Estimate of quantity of each type of asset.

For each asset rendered, give either a good faith estimate of market value OR historical cost when new & the year acquired for the asset(s). This helps to accurately depreciate the items.

All assets rendered must have a value. Items received as gifts, or used assets where the historical cost or year acquired is not known should be listed with a good faith estimate of market value.

Fiduciaries will need to list the property owner’s name and address in the last column.

If more space is needed to list your assets, it is permissible to attach supplement pages, additional sheets, or excel spreadsheets with the required information as necessary.

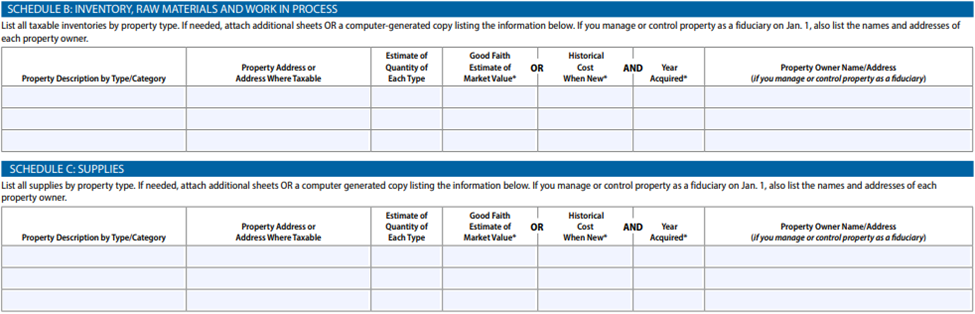

Schedule B & Schedule C: Inventory, Raw Materials and Work in Progress/Supplies

Schedule B and C are required if the total value of all property exceeds $20,000 and own the type of property described in the heading.

Schedule B: list only inventory, raw materials, and work in progress.

Schedule C: list only supplies.

Similar to Schedule A, Schedule B and C requires a list of the property type/category, an estimate of quantity for each type, and either a good faith estimate of market value OR historical cost when new & the year acquired for the asset(s).

All assets rendered must have a value. Items received as gifts, or used assets where the historical cost or year acquired is not known should be listed with a good faith estimate of market value.

If inventory, raw materials, work in progress, and/or supplies have already been listed under Schedule A, you do not need to add them under Schedules B or C.

The taxable location, the property address, must also be listed for each type (if different from situs listed in Section 1).

Fiduciaries will need to list the property owner’s name and address in the last column.

If more space is needed to list your assets, it is permissible to attach supplement pages, additional sheets, or excel spreadsheets with the required information as necessary.

Schedule D: Vehicles and Trailers and Special Equipment

Schedule D is required if the total value of all property exceeds $20,000 and you have property that fits the description under schedule D.

The Year, Make, Model, and Vehicle Identification Number (VIN) of each vehicle is optional, but very useful to determine an accurate value & and ensure there is no double assessment.

All vehicles rendered must include either a good faith estimate of market value OR historical cost when new & the year acquired for the asset(s).

All assets rendered must have a value. Items received as gifts, or used assets where the historical cost or year acquired is not known should be listed with a good faith estimate of market value

If vehicles have already been listed under Schedule A, you do not need to add them under Schedule D.

If more space is needed to list your assets, it is permissible to attach supplement pages, additional sheets, or excel spreadsheets with the required information as necessary.

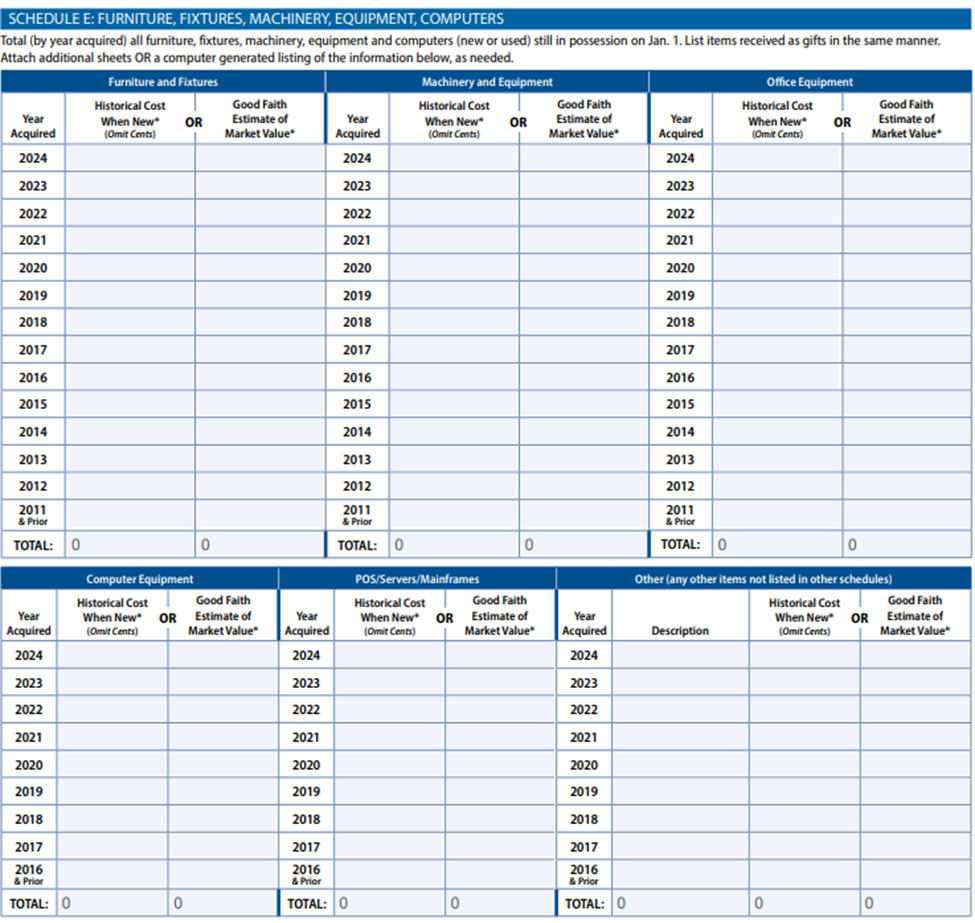

Schedule E: Furniture, Fixtures, Machinery, Equipment, Computers, POS, Other

This section breaks down the type of personal property by year acquired.

In each section, you will provide the historical cost when new in the corresponding year acquired column OR a good faith estimate of market value per asset year.

All assets rendered must have a value. Items received as gifts, or used assets where the historical cost or year acquired is not known should be listed with a good faith estimate of market value.

Add Totals of Historical Cost or Good faith estimate of value for each column as applicable.

There is also an “Other” column for any items owned by the business that were not listed in any other section. Could include signage.

If more space is needed to list your assets, it is permissible to attach supplement pages, additional sheets, or excel spreadsheets with the required information as necessary.

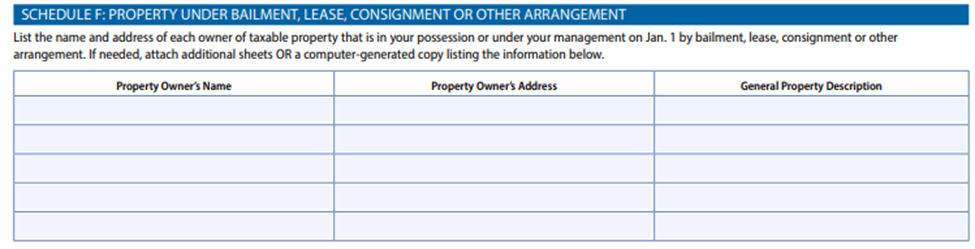

Schedule F: Property Under Bailment, Lease, Consignment or Other Arrangement

This section should be completed by any business that possesses this type of property regardless of its total market value of all business personal property.

If the business is using personal property assets that are under bailment, lease, consignment or other arrangement where the business is not responsible for the business personal property taxes, list the property here.

Include the owner’s name, address, and a general description of the property.

The district may ask the business owner to provide additional information, including lease agreements, rental prices, contracts, etc.

If more space is needed to list your assets, it is permissible to attach supplement pages, additional sheets, or excel spreadsheets with the required information as necessary.

The last page of the rendition contains important information about deadlines, filing instructions, penalties, as well as definitions of common terms that will help users more fully understand the requirements.

Please contact the Comal Appraisal District Business Personal Property department for any additional questions or clarifications.

What You Need To Know About Starting A Dealership

Motor Vehicle Inventory Tax Statement (VIT) and Inventory Declaration (Declaration)

Within 30 days of the active date of your license, (not when you open for business or start selling vehicles), notify both the county tax office and the appraisal district that you are a new dealer, where the dealership is located, and request to set up an account.

VIT: A VIT reports information on vehicles sold in the previous month. File these at both the county tax office and the appraisal district. If no sales are made, you must file the form reporting zero sales. If filed late, penalties may be assessed. (Most often due on the 10th day of each month, check with your county for details.)

Declaration: A Declaration reports the total number of sales made during the previous year. File these at both the county tax office and the appraisal district. If no sales are made, you must file the form reporting zero sales. If filed late, penalties may be assessed. (Due between January 1 – February 1 of each year)

Minimum Vehicle Sales

You must remain regularly and actively engaged in business by selling or assigning at least 5 vehicles in a calendar year or the license may be revoked or canceled.

Association Websites

Franchise: Texas Auto Dealers Association: www.tada.org

Where do I send the Dealer’s Inventory Declaration and Monthly Vehicle Inventory Tax Statements?

Declarations: Mail the original to the appraisal district and a copy to the tax assessor-collector.

Monthly Statements: Mail the original along with your payment to the tax assessor-collector and a copy of the statement to the appraisal district.

Comal Appraisal District – You may submit your tax statement by mail to 900 S SEGUIN AVE, NEW BRAUNFELS, TX 78130, by fax to (830)625-8598, or by email at CADBPP@co.comal.tx.us.

Comal County Tax Assessor-Collector- 205 N Seguin Ave., New Braunfels, Texas 78130 (Tax Office phone number for questions: 830-221-1353)

When are the Monthly VIT Statements and Annual Declarations due?

Dealers Motor Vehicle Inventory Tax Statements are due on or before the 10th of each month.

A declaration must be filed not later than February 1 of each year or, in the case of a dealer who was not in business on January 1, not later than 30 days after commencement of the business, except as provided by Texas Property Tax Code Section 23.122(l). A dealer is presumed to have commenced business on the date of issuance of their general distinguishing number as provided by Transportation Code Chapter 503. Notwithstanding this presumption, a chief appraiser may, at their sole discretion, designate another date on which a dealer commenced business.

How is Dealer Inventory appraised?

Although dealers are required to report and pay inventory tax on sales into an escrow account with the tax assessor-collector, the law requires that a market value be assigned to dealer inventory based on the previous year’s sales. The market value assigned is equal to 1/12 of the total dollar amount of sales from the previous year minus dealer, fleet, and subsequent sales.

I paid into escrow on each sale during the year, why do I owe more taxes?

Your escrow payments are based on the sales in the current year, but your tax is based on the prior year sales. Therefore, If the current year sales are less than the prior year sales you will owe more than you have placed in escrow.

What is the Declaration and when is it due?

The Declaration is an annual report of your prior year’s sales and determines your market value for the current year. It is due every year prior to February 1. New dealers with licenses issued after January 1 of the current year are required to file a Declaration with the appraisal district and assessor-collector within 30 days of the date that the dealer license was issued by the state.

What is the Dealer Inventory Tax Statement and when is it due?

The Inventory Tax Statement is a report of your prior months sales and indicates the calculation of the Unit Property Tax on those sales. The statement is due by the 10th of every month for Motor Vehicle, Vessel/ Outboard Motors, and Manufactured Housing Dealers. Heavy Equipment Dealers have until the 20th of each month to submit Dealer Inventory Tax Statements.

Is there a fine or penalty for not filing the Annual Declarations or Monthly Statements?

Yes, please refer to the penalties listed on your Inventory Declaration Form and the Monthly Inventory Tax Statement.

I was issued a dealer number but did not own any vehicles on January 1st. Am I still required to file the Declaration and Statements?

Yes, you are considered in business beginning on the date the dealer number is issued and continuing until it is canceled or expires.

Why do I have to file forms each month even if I did not have any sales or own inventory?

The law requires dealers to file every month that your dealer number is active even if you do not have sales or inventory. If you have not made any sales in the prior month, complete steps 1-2 and write “No Sales” in step 3 and sign and date the form.

Am I required to complete a Business Personal Property Rendition form (Form 50-144)?

Yes, all dealers must render their parts, accessories, supplies, and fixed assets used in the business. The assets reported on the rendition will have a separate account number. Do not include your vehicle inventory in the rendition.

Can I send in a computer listing of sales or substitute a report from my dealer software system?

Yes. You may complete steps 1, 2, 4, and 5 of the Statement form and attach a sales listing, as long as the listing includes all information required in step 3. You may also submit a report generated by your dealer software system in place of the Statement form if it contains all the required information.

If all sales are wholesale (dealer to dealer), do I have to file?

If your license type allows you to sell at the retail level you are required to file, regardless of the type of sale.

If I take an even trade, how is the transaction reported?

Sales price means the total amount of money paid or to be paid for the purchase of a motor vehicle. It is the same amount as the “sales price” on line 21 of the form entitled “Application for Texas Certificate of Title.” In a transaction that does not involve the use of that form, the term means an amount of money that is equivalent or substantially equivalent to the amount that would appear on line 21 as the “sales price” on the application for Texas Certificate of Title.

Are consignment sales a part of my inventory?

Yes, in the case of dealer inventory, the definition of inventory includes all vehicles held for sale by a dealer. See Tax Code 23.121(b) and (a)(4). What this means is that any sale by a dealer, regardless of ownership or consignment status, is counted as inventory for tax purposes. Therefore, consignment sales must be reported on the Monthly Inventory Tax Statement and Annual Declaration.

What is considered heavy equipment?

Texas Property Tax Code Section 23.1241(a)(6) defines heavy equipment as any item of equipment that is:

self-propelled, self-powered, or pull-type equipment, including farm equipment or a diesel engine

weighs at least 500 pounds, and is intended to be used for agricultural, construction, industrial, maritime, mining, or forestry uses

is not a motor vehicle that is required to be titled or registered.

Is sales tax included in the sales price of heavy equipment or in the monthly lease or rental payment, as applicable?

Yes, the sales price is part of the total price paid for the equipment and is included in the sales tax.

The sales price of heavy equipment is defined in Texas Property Tax Code Section 23.1241(a)(7) as the total amount of money paid or to be paid to a dealer for the purchase of an item of heavy equipment (or for a lease or rental with an option to purchase), the total amount of the lease or rental payments, plus any final consideration, excluding interest. The sales price includes the sales tax since it is part of the money paid or to be paid to a dealer for the purchase of the heavy equipment.

Is anyone who sells, leases or rents heavy equipment a dealer? Or must the person be engaged in the business in this state of selling, leasing or renting heavy equipment?

Texas Property Tax Code Section 23.1241(a)(1) defines a dealer as a person engaged in this state in the business of selling, leasing, or renting heavy equipment. A dealer engaged in business in Texas that sells or leases heavy equipment must be permitted to collect state and local sales tax since these are taxable transactions for sales tax purposes. An appraisal district can verify if the person has a Texas sales tax permit.

Business personal property is composed of fixed assets and inventory. Business personal property includes, but is not limited to, furniture, equipment, tools, machinery, computers, copiers, motor vehicles, raw materials, goods in process, finished goods (awaiting sale or distribution), and inventory held for sale on consignment.

Please note: If you use your own personal tools, machinery, equipment, vehicles or any other item, gadget or thing to produce a product or provide a service and receive income, those items are included in the appraisal assessment.

What is a rendition for Business Personal Property?

A rendition is a form that provides the appraisal district with the description, location, cost and acquisition dates or a “Good Faith Estimate of Value” for business personal property that you own. The appraisal district uses the information to help estimate the market value of your property for taxation purposes.

The Texas Property Tax Code does not require Appraisal Districts to mail out renditions. Comal AD does this as a service, but it is the responsibility of the taxpayer to complete and submit a rendition each year. You can find the rendition form on our website.

Who must file a rendition?

A person who owns tangible personal property used for the production of income that the person owns or manages and controls as a fiduciary on January 1.

Do I have to file a Rendition Form for my business?

Yes, Renditions are due April 15th. A penalty of 10% of the tax liability will be imposed for failure to file a timely rendition.

What must the rendition statement contain?

Property owner’s name and address

Description of the property by type or category (fixed assets)

Description and quantity of each type of inventory Property’s physical location or taxable situs

Property owner’s option of providing either a “good” faith estimate of market value or historical cost new and year of acquisition of individual items

Property owner’s signature or signature of employee or tax agent

What information is required for the rendition?

Depending on the type of property you own and its value, you can expect to provide the following information:

Location

You will need to give the address where the property was located on January 1. If the property was in transit on January 1, or is regularly used in more than one location, you should provide additional information about the property’s normal location and circumstances on January 1.

General description

A general description should give enough information to identify the property and distinguish it from other items that you own. At minimum, you should identify the major categories of personal property assets that you own, using the same terminology you would use in reporting to the internal revenue service. You have the option of providing an itemized listing of the various assets in any category. For vehicles, you will need to provide the plate and VIN number, as well as the year, make, and model.

Quantity of items

If you own an inventory of items that you hold for sale or rental, you will need to provide an estimate of the quantity of each type of item that you hold in inventory. Again, you can provide an itemized list if you prefer for any category. Good faith estimate of market value The appraisal district will estimate the market value of your items on the basis of your rendition and other information in its possession. Under the rendition law, you must include in your rendition either a good faith estimate of the market value of your items or the historical cost and acquisition date (discussed below) of the items, if the value of your items are $20,000 or more. If you choose to give a market value estimate, you should be aware that there are several different definitions of market value that may apply. For items other than inventory, market value is defined as follows: “Market value” means the price at which a property would transfer for cash or its equivalent under prevailing market conditions if:

exposed for sale in the open market with a reasonable time for the seller to find a purchaser;

both the seller and the purchaser know of all the uses and purposes to which the property is adapted and for which it is capable of being used and of the enforceable restrictions on its use; and

both the seller and purchaser seek to maximize their gains and neither is in a position to take advantage of the exigencies of the other. (Sec. 1.04, Texas Tax Code).

For inventory, market value is defined by the tax code as “the price for which it would sell as a unit to a purchaser who would continue the business.” Sec. 23.12, Texas Tax Code. If your business has 50 or fewer employees, you may base your estimate of value on federal income tax depreciation schedules. You will need to be prepared to defend your estimate and explain how it was developed.

Original cost

Instead of providing a good faith estimate of market value, you may provide the original cost and date you acquired the property. Original cost (the code uses the term “historical cost when new”) refers to the amount you paid to acquire the property. Your cost would include transportation and any other necessary expenses incurred in acquiring the property. If you purchased a used item, you should note on the form that you purchased it used and give the amount you paid.

Date of acquisition

Date of acquisition is simply the date you bought or acquired ownership of the property.

Click here for more information about How to Complete a Business Personal Property (BPP) Rendition

My business has an aggregate value less than $20,000. Must I complete all of this complicated form?

Personal property used for business purposes must be reported, so you will have to file at least the general rendition form. However, you will only be required to fill out a short table generally describing your assets and giving their location.

If the total fair market value of your business assets, including any vehicles, inventory, supplies, are less than

$20,000, you may check the under $20,000 box in Step 5. You have two options:

Option 1 is to fill out Schedule A, and where applicable, Schedule F.

Option 2 is to fill out Schedule C and E and, where applicable, B, C, D and F.

What if I move or sell my business during the year?

The tax liability on business personal property is determined as of January 1 of each tax year. Therefore the property is taxed according to its location and ownership as of January 1.

What if I close my business during the year, will my taxes be prorated?

No, the taxes will be assessed for the entire year.

Is leased equipment taxable?

Yes, it is taxable to the owner of the property as of January 1 of the tax year. Operational leases of equipment or vehicles are reported on Schedule F. Note: If the lease is a capital lease, you may be responsible for reporting the asset. If you take depreciation on your federal tax return, then you must report the asset in either Schedule A or Schedule E unless your lease contract states that the asset will be reported by the lessor (Lease Company).

Is my business taxable if I operate it from my home?

Yes, all business assets, regardless of location, are taxable.

How do I determine Original Cost?

To determine original cost, refer to your accounting records, such as original journal entries and account ledgers. Use original purchase documents, such as invoices or purchase orders, to determine the original cost of the asset. Add all costs attributed to getting the asset functioning, such as freight and set-up cost.

What is Inventory? What does that include?

Merchandise (goods in the hands of a wholesaler or retailer that is ready for sale), raw materials, finished goods and work in process. Inventory should be reported at your cost.

What kind of supplies should be reported?

Supplies are typically items that are expensed in your business throughout the year such as office supplies, business cards, shop supplies, etc. You will need to provide the actual or estimated cost supplies that were on hand as of January 1.

May I use my bookkeeping records as my rendition?

Yes. Attach these records to the rendition, sign and date it and then return it to our office. Include asset listings with the date of acquisition and original cost. All assets owned by the business must be rendered.

If all my business personal property has already been depreciated out according to Federal Income Tax Laws, is my business still taxable?

Yes, if your business personal property is still in use and used to generate income, your business personal property is taxable.

What if I don’t have business assets to report?

All businesses have some taxable assets, from desks and chairs, a computer, and/or supplies.

What happens if I do not file a rendition, or file it late?

If you do not file a rendition, the appraised value of your property will be based on an appraiser’s estimate by comparing business types and conducting field inspections. In addition, if you fail to file your rendition before the deadline or you do not file it at all, a penalty equal to 10% of the amount of taxes ultimately imposed on the property will be levied against you. There is also a 50% penalty if a court finds you engaged in fraud or other actions with the intent of evading taxes. If you fail to file a rendition and subsequently file a protest, you bear the burden of proof at the Appraisal Review Board hearing.

When and where must the rendition be filed?

The first day to file is after January 1st and the last day to file your rendition is April 15th annually. If you mail your rendition, it must be postmarked on or before April 15th. You may hand deliver your rendition to our office on or prior to April 15th. You may also fax or e-mail your rendition on or prior to April 15th.

You may mail or deliver your renditions to the Comal Appraisal District:

900 S. Seguin Ave, New Braunfels TX 78130 Fax: (830) 625-8598

How do I find out whether the appraisal district received my rendition on time?

Call our office at (830) 625-8597 and ask for the Business Personal Property department

If I cannot file the rendition on time, what should I do?

The law provides for a 30-day extension of time to file a rendition if the taxpayer makes the request in writing on or prior to April 15th.

Can I report all my properties on one rendition?

If the appraisal district has already set up accounts covering your property, you should file a rendition corresponding to each account. If the district does not have accounts set up for your property, it is generally best to file a rendition applicable to each location where your property is kept. For example, if you own three separate convenience stores, file three renditions, one for each store.

Can I request an extension to file the rendition?

Yes. See what to do if you can’t file on time, above.

If I can’t file by the extension deadline, what should I do?

You should file your rendition as soon as you can and include with it a request for waiver of penalty and explanation of your reasons for missing the deadline as described above. If you receive a notice from the chief appraiser regarding the imposition of a penalty, be sure to file the request for waiver within 30 days of the date you receive it. For more information, contact the Comal Appraisal District at (830) 625-8597 or cadbpp@co.comal.tx.us. The district’s website is www.comalad.org.

Does a non-profit organization automatically receive a property tax exemption for Business Personal Property owned by the organization?

No, often organizations mistakenly believe they are entitled to a property tax exemption because they have received a federal income tax exemption under Section 501(c) (3) of the Internal Revenue Code or an exemption from State sales taxes. The constitution requirements for property tax exemptions are different than the provisions covering income and sales taxes. A non-profit organization may qualify for a total exemption from property taxes, but they must apply for the exemption by April 30.

Can I receive a copy of last year’s rendition form?

These forms are confidential. Per Sec. 22.27 of the Property Tax Code, disclosure is only permitted to the person who filed the statement or report, or the owner of the property subject to the statement, report or information, or the agent authorized to receive the information.

I rendered my business personal property last year and nothing has changed. Do I still need to fill out the rendition form?

Yes. If your personal property assets on January 1, were exactly the same as those assets contained in your most recent rendition statement you have filed with the appraisal district, then all you need to do is check the affirmation box in Part 3 on page 1 on your rendition form. After checking the affirmation box in Part 3, complete the Signature and Affirmation box at the bottom of the page.

What will the appraisal district do with my rendition?

Your rendition will be analyzed and used; along with other information we collect on similar businesses, to develop an estimate of value for your property.

Is my information confidential?

Yes. Information contained in a rendition cannot be disclosed to third parties except in very limited circumstances. In addition, the code specifically provides that any estimate of value you provide is not admissible in proceedings other than a protest to the ARB or court proceedings related to penalties for failure to render. The final value we place on your property is public information, but your rendition is not.

How should I estimate market value?

Publications that provide value information on assets are helpful tools in estimating market value. For example, there are numerous publications on vehicles and computer equipment that provides a range of value information for these assets. If you choose to use published value information, you must use a value that would reflect the assets worth near January 1st. You can use CAD’s published Business Personal Property Value Calculation Guidelines, which is posted on our web site at www.comalad.org. Developing an estimated useful life and replacement cost of an asset is another method of estimating market value. Divide the actual age of the asset by the estimated useful life in order to calculate the depreciation for the asset. Multiply the depreciation percentage by the replacement cost to estimate an amount of depreciation. Subtract the amount of depreciation from the replacement cost to arrive at an estimate of market value. If your business has 50 employees or less, subsection 22.07(c) allows you to base your good faith estimate of market value on depreciation schedules used for federal income tax purposes.

How should I determine original cost?

To determine original cost, you need to refer to your accounting records, such as original journal entries and account ledgers. Use original purchase documents, such as invoices or purchase orders to determine the original cost of the asset. You need to add all cost that is attributed to getting the asset functioning, such as freight and set-up cost.

What are the penalties for failure to comply?

There are two levels of penalties for failure to comply. If you fail to file your rendition or explanatory statement before the deadline or you do not file it at all, the penalty is equal to 10% of the amount of taxes ultimately imposed on the property. If a court determines that you have committed fraud or done other acts with the intent of evading taxes on the property, a penalty equal to 50% of the taxes ultimately imposed on the property will be levied. The penalty will be a separate line item on your tax bill.

What are my rights if a penalty is assessed against me?

If a rendition penalty is assessed against you, you can file a request for a waiver of the penalty. You must file the request in writing with the chief appraiser within 30 days after you receive the notice that the penalty has been imposed. Your request must include documentation showing that either you substantially complied with the rendition law or that you made a good faith effort to do so. The documentation should also address:

your compliance history with respect to paying taxes and filing statements or reports;

the type, nature, and taxability of the specific property involved;

the type, nature, size, and sophistication of the person’s business or other entity for which property is rendered;

the completeness of your records;

your reliance on advice provided by the appraisal district that may have contributed to your failure to comply and the imposition of the penalty;

any change in appraisal district policy during the current or preceding tax year that may affect how property is rendered; and

any other factors that may have caused you to fail to timely file a statement or report.

The chief appraiser is required by law to consider these factors and notify you in writing. If the chief appraiser declines to waive a penalty and you have made a timely request for waiver, you may protest the imposition of the penalty to the appraisal review board. The board may waive the penalty if it finds that you substantially complied with the rendition law or made a good faith effort to do so.

When can the chief appraiser request an explanatory statement from me?

If you provide a good faith estimate of market value instead of original cost and acquisition date for any items, the chief appraiser may request an explanatory statement from you. The chief appraiser must make the request in writing, and you must provide the statement within 21 days of the date you receive the chief appraiser’s request.

What must I include in an explanatory statement?

The explanatory statement must set out a detailed explanation of the basis for the estimate(s) of market value given in your rendition. The statement must include adequate information to identify the property. It must describe the physical and economic characteristics of the property that are relevant to its market value. It must give the source(s) of information used in valuing the property and explain the basis for the value estimate.