A property tax exemption reduces the taxable value of your property which lowers your taxes. For example, if your home is valued at $100,000 and you qualify for a $20,000 exemption, you only pay taxes on $80,000.

A “Partial” exemption excludes a part of the value from taxation and can exclude all of the value of a property from taxation if the exemption amount exceeds the market value (i.e., homestead exemption). An “Absolute” or “Total” exemption excludes the entire value from taxation (i.e., churches).

Homeowner Exemptions

Residence Homestead Exemption

A homestead exemption helps you save on taxes for your home. An exemption reduces the taxable value of your property from taxation and lowers your taxes. For example, if your home is valued at $100,000 and you qualify for a $20,000 exemption, you pay taxes on your home as if it was worth only $80,000.

What Kinds of Homestead Exemptions Are Available?

- School taxes — all homeowners. If you qualify for the homestead exemption, you will receive at least $140,000 homestead exemption on the value of your home for school district taxes.

- County taxes — all homeowners. Comal County currently provides a 20% local option homestead exemption to all homeowners. This means, for example, that if your home is valued at $100,000, the exemption will reduce its taxable value for Comal County taxes by $20,000 to $80,000.

- Optional exemptions — all homeowners. Any taxing unit, including a school district, city, county or special district, may offer a local option exemption for up to 20% of your home’s value. The amount of an optional exemption can’t be less than $5,000, no matter what the percentage is. For example, if your home is valued at $20,000 and your city offers a 20% optional exemption, your exemption is $5,000, even though 20% of $20,000 is just $4,000. The governing body of each taxing unit decides whether it will offer the exemption and at what percentage. This percentage exemption is added to any other homestead exemption for which the applicant qualifies.

You must own and occupy your home on the date you request the exemption and may not claim a homestead exemption on any other property. If you temporarily move away from your home, you still can qualify for this exemption, if you do not establish another principal residence and you intend to return in less than two years. You may exceed the two-year limit if you are in military service serving outside of the United States or live in a facility providing services related to health, infirmity or aging. Applications cannot be filed before the date you qualify for the exemption.

Effective January 1, 2022, a property owner who acquired property after January 1 may receive the residence homestead exemption for the applicable portion of that tax year upon qualification, if the previous owner did not receive the same exemption for that tax year.

Each individual owner, excluding married couples, residing on the property must complete a separate application to qualify for an exemption for his or her interest in the property. If separate individuals own this property, you must list the percent of ownership for each and the name and mailing address of each owner who does not reside at the property. Exemptions are allocated according to percent of ownership interest the applicant has in the property. For property owned through a beneficial interest in a qualifying trust, attach a copy of the document creating the trust. For heir property, see ____ for required documents.

Over-65 Homestead Exemption

A person who is 65 or older may receive additional exemptions. You are eligible for these exemptions as soon as you turn 65; you don’t need to be 65 as of the first of the year to apply. If we have your birthdate on file, we will automatically grant the Over-65 exemption. If not, you will need to submit a new application.

School districts automatically grant an additional $60,000 exemption for qualified persons who are 65 or older. An additional advantage of the Over-65 exemption is the school tax ceiling. Once you qualify, your school taxes will not increase unless you make improvements to the home.

Cities, the county, and other taxing units may, but are not required to, offer Over-65 homestead exemptions of at least $3,000 and sometimes much more. Click here to determine what taxing units in where your home is located offer an over-65 homestead exemption.

If you qualify for the Over-65 Exemption, there is a property tax “ceiling” that automatically limits School taxes to the amount you paid in the year that you qualified for the homestead and the Over-65 exemption. A County, City, or Junior College may also limit taxes for the Over-65 Exemption if they adopt a tax ceiling. Tax ceiling amounts can increase if you add improvements to your home (i.e., adding a garage, room, or pool). In addition, Over-65 homeowners who purchase or move into a different home in Texas may also transfer a percentage. This is commonly referred to as a Transfer Ceiling Certificate or Port.To transfer your tax ceiling for the purposes of County, City, or Junior College District taxes, however, you must move to another home within the same taxing unit. You must request a certificate from the Appraisal District for the former home and take it to the Appraisal District for the new home, if located a different district.

You may not receive both the Over-65 and Disabled Person exemption from the same taxing unit in the same tax year, however, you may receive both exemptions from different taxing units. Please contact the Appraisal District if you believe you qualify.

Surviving Spouse of Person Who Received the Over-65 Exemption

If qualified, a Surviving Spouse may continue to receive the Over-65 exemption and the tax ceiling. To qualify, your deceased spouse must have been receiving the Over-65 exemption on the residence homestead or would have applied and qualified before the spouse’s death. The Surviving Spouse must have been age 55 or older on the date of the spouse’s death. You must have ownership in the home and proof of death of your spouse.

Disabled Person Homestead Exemption

In Texas, a disabled adult has a right to receive an additional exemption. If you qualify, this exemption can reduce your tax liability.

School districts automatically grant an additional $60,000 exemption for qualified persons who are disabled. An additional advantage of the disabled exemption is the school tax ceiling. Once you qualify, your school taxes will not increase unless you make improvements to the home.

Cities, the county, and other taxing units may, but are not required to, offer disabled homestead exemptions of at least $3,000 and sometimes more. Click here to determine what taxing units in where your home is located offer a disabled homestead exemption.

The Texas Property Tax Code provides that you are entitled to the Disabled Person exemption if you meet the Social Security Administration’s tests for disability. In simplest terms:

- You must have a medically determinable physical or mental impairment;

- The impairment must prevent you from engaging in any substantial gainful activity; and

- The impairment must be expected to last for at least 12 continuous months or to result in death.

Alternatively, you will qualify if you are 55 or older and blind and you cannot engage in your previous work because of your blindness.

To automatically qualify, you must meet the Social Security definition for disabled and receive disability benefits under the Federal-Old Age, Survivors and Disability Insurance Program administered by the Social Security Administration. To verify your eligibility, you must provide a current dated statement from the Social Security Administration showing that you are disabled and the date your disability began.Disability benefits from any other program do not automatically qualify you for this exemption.

You do not have to receive disability benefits to qualify, but you must meet the Social Security definition for disabled. If you are not receiving Social Security benefits, then you must have your physician complete the CAD “Physician’s Statement” form available on this site or you may contact Customer Service at (830) 625-8597 option 1.

Disability benefits from any other program, including a disabled veterans’ pension, do not automatically qualify you for this exemption. You may need information on disability ratings from the civil service, retirement programs or from insurance documents, military records or a doctor’s statement. Also read information about the disabled veterans’ exemption.

If you qualify for the Disability Exemption, there is a property tax “ceiling” that automatically limits School taxes to the amount you paid in the year that you qualified for the homestead and Disability exemption. A County, City or Junior College may also limit taxes for the Disability Exemption if they adopt a tax ceiling. Tax ceiling amounts can increase if you add improvements to your home (i.e., adding a garage, room or pool.) In addition, Disabled homeowners who purchase or move into a different home in Texas may also transfer the percentage of School taxes paid, based on the former home’s school tax ceiling. This is commonly referred to as a Ceiling Transfer. To transfer your tax ceiling for the purposes of County, City or Junior College District taxes, however, you must move to another home within the same taxing unit. You must request a certificate from the appraisal district for the former home and take it to the appraisal district for the new home, if located in a different district.

You may not receive both the Over-65 and Disabled Person exemption from the same taxing unit in the same tax year, however, you may receive both exemptions from different taxing units. Please contact the Appraisal District if you believe you qualify.

Surviving Spouse of Person Who Received the Disability Exemption

If qualified, a Surviving Spouse may continue the spouse’s tax ceiling. To qualify, your deceased spouse must have been receiving the Disabled Person exemption on the residence homestead. The Surviving Spouse must have been age 55 or older on the date of the spouse’s death. You must have ownership in the property and proof of death of your spouse. You may contact the Customer Service department for additional information at (830) 625-8597 option 1.

Residence Homestead Exemption for Disabled Veteran with 100% Disability

To qualify for this, you must submit a Homestead Exemption application accompanied with a current copy of your V.A. award letter or other document from the United States Department of Veterans Affairs showing 100 percent disability compensation due to a service-connected disability and a rating of either 100 percent disabled or individual unemployability.

A surviving spouse may qualify for the 100% Disabled Veteran Homestead Exemption.

Surviving Spouse of Disabled Veteran who qualified for Donated Residence Homestead

A disabled veteran is allowed an exemption equal to his or her disability rating (if less than 100 percent) on a residence homestead donated by a charitable organization. The same percentage exemption extends to the surviving spouse if certain conditions are met.

Surviving Spouse of Member of Armed Forces Killed in Line of Duty, or Surviving Spouse of First Responder Killed in Line of Duty

A surviving spouse of a member of the U.S. armed services killed in action or a surviving spouse of a first responder killed in the line of duty is allowed a total property tax exemption on his or her residence homestead if the surviving spouse has not remarried since the death of the armed service member or of the first responder.

Heir Property

Homeowners who have inherited their home may qualify for a homestead exemption on 100% of the property value due to a new Texas law enacted in 2019 makes it easier for heir property owners to qualify for a homestead exemption by creating more accessible application requirements.

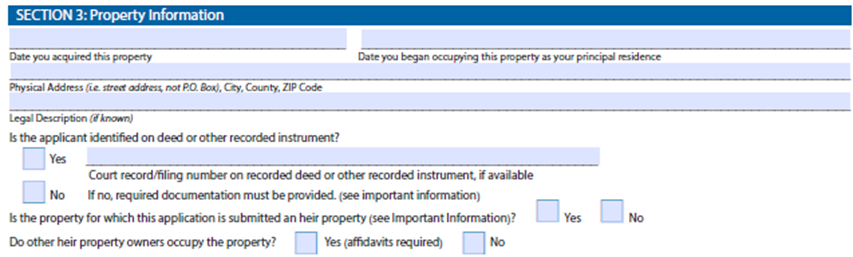

Heir Property is property owned by one or more individuals, where at least one owner claims the property as a residence homestead, and the property was acquired by will, transfer on death deed, or intestacy. An heir property owner not specifically identified as the residence homestead owner on a deed or other recorded instrument in the county where the property is located must provide:

- An affidavit establishing ownership of interest in the property

- A copy of the property owner’s death certificate;

- A copy of the property’s most recent utility bill; and

- A citation of any court record relating to the applicant’s ownership of the property, if available.

Each heir property owner who occupied the property as a principal residence, other than the applicant, must provide an affidavit that authorizes the submission of the application.

11.35 Disaster Exemption

A property may qualify for a temporary exemption for a qualified property damaged by a disaster within 105 days that the Governor declares a disaster and at least 15% of the improvement is physically damaged by the disaster. Section

11.35 of the Texas Property Tax Code outlines the properties that qualify for this temporary exemption and the actions needed to be undertaken by the property owner/agent to apply and qualify for the 11.35 (Disaster) exemption.

Other Exemptions

Disabled Veteran or Survivors of a Disabled Veteran

You may qualify for a property tax exemption if you are either (1) a veteran who was disabled while serving with the U.S. armed forces or (2) the surviving spouse or child (under 18 years of age and unmarried) of a disabled veteran or of a member of the armed forces who was killed while on active duty. You must be a Texas resident.

To establish eligibility, you must have documents from either the Veterans’ Administration or the branch of the armed forces that shows the percentage of your service-related disability. Your disability rating must be at least 10 percent.

If you are a surviving spouse or child, you must have the veteran’s disability records. You may need other documents such as proof of marriage or age.

Currently, the exemption ranges from $5,000 to $12,000, depending on the extent of the disability. This exemption is not only for a home — you can apply it to any property you own on January 1, such as to a truck used for business purposes. However, you may pick only one property to receive this exemption. The appropriate exemption amount will be deducted from the appraised value of the property to which you want the exemption applied.

The disabled veterans’ exemption is different from a disabled homeowner’s exemption, and disabled veterans do not necessarily qualify for the latter type exemption.

This chart outlines disabled veterans’ exemptions effective January 1, 2008:

You may qualify for this exemption if you are a veteran of the U.S. Armed Forces and your service branch or the Veterans Administration has officially classified you as disabled with a percentage of 10% or more. You must be a Texas resident. Your application can apply to any one property you own on January 1 on which property taxes are assessed. You must complete an application and attach a copy of a current dated letter from the Veterans Administration reflecting the percent of disability awarded. You must file the application by April 30 or late file no later than five years after the delinquency date. A surviving spouse or child may also qualify to continue this exemption; a surviving spouse may continue the exemption if the survivor does not remarry. When the disabled veteran attains age 65, is totally blind in one or both eyes, or has lost the use of one or both limbs, they will qualify for 100% of the maximum exemption amount of $12,000 offered regardless of the disability percentage awarded by the V.A.

A surviving spouse or child of an armed forces member killed on active duty may qualify for this exemption. The surviving child, under age 18 and unmarried, or surviving spouse must be a Texas resident. An application must be completed along with a letter from the Veterans Administration showing the person died while on active duty, copy of your marriage license; a surviving child must attach a copy of proof of age and relationship to the deceased.

Tax Deferral for 65 or Older or Disabled Homeowner

If you meet the definition of disabled given above and/or are age 65 or older, the law gives you an additional right. Disabled persons can defer, or postpone, paying current and delinquent property taxes on their homestead for as long as they own it and live in it. The tax deferral applies to taxes owed to all taxing units that tax the homestead property. To postpone tax payments, you must file a Tax Deferral Affidavit with the Comal Appraisal District.

You should be aware that tax deferral only postpones the payment of the taxes owed, it does not cancel them. Taxes will continue to add up, and they accrue interest at the rate of 5% per year. As soon as you cease to own the home or live in it, all taxes, penalties, and interest become delinquent if not paid within 180 days. The taxing units may proceed with delinquent tax suits if the taxes remain unpaid.

A homeowner is eligible to file a tax deferral as soon as he or she meets the definition given above. There is no need to wait until the next January 1 to be eligible. Affidavit forms are available in our information center or on this website (insert link). Our office notifies Tax Office that you have filed it.

Note: If you have an existing mortgage on your residence, the tax deferral does not prevent your mortgage

company from paying delinquent taxes; a tax deferral applies only to the collection of taxes.

Charitable Exemption

An organization that qualifies as a charitable organization is entitled to certain exemptions from taxation. To qualify, the organization must be organized exclusively to perform religious, charitable, scientific, literary, or educational purposes, engage exclusively in performing one or more of many charitable functions. A charitable organization must be operated in a way that does not result in accrual of distributable profits, realization of private gain resulting from payment of compensation in excess of a reasonable allowance for salary or other compensation for services rendered, or realization of any other form of private gain, and some charitable organizations must be organized as a non-profit corporation as defined by the Texas Non-Profit Corporation Act. See the Texas Property Tax Code in Section 11.18 for more details (link available on this site). The application is available on this site, or you may contact Customer Service at (830) 625-8597 option 1.

Religious Exemption

An organization that qualifies as a religious organization is entitled to certain exemptions from taxation. To qualify, the organization must be organized and operated primarily for the purpose of engaging in religious worship or promoting the spiritual well-being of individuals. The organization must be operated in such a way that no individual profits (other than salary) and the organization’s bylaws, charter or other regulations must pledge its assets for use in performing the organization’s religious functions. See the Texas Property Tax Code in Section 11.20 for more details (link available on this site). The application is available on this site or you may contact Customer Service at (830) 625-8597 option 1.

Agricultural / Wildlife / Special Appraisal

Land designated for agricultural use is appraised at its value based on the land’s capacity to produce agricultural products. The value of land based on its capacity to produce agricultural products is determined by capitalizing the average net income the land would have yielded under prudent management from production of agricultural products during the five (5) years preceding the current year. Property owners may qualify for agricultural appraisal under two different laws. You may refer to Subchapter C, Section 23.41 and Subchapter D, Section 23.51 of the Texas Property Tax Code (link available on this site) for details of these laws or you may consult with the appraisal district. The open-space land (1-d-1) application is available on this site or you may contact Customer Service at (830) 625-8597 option 3.

Freeport Exemptions for Business Personal Property

Material that is transported outside of this state not later than 175 days after the date the person who owns it on January 1 acquired it, or imported it into this state, and assembled, manufactured, repaired, maintained, processed, or fabricated and shipped the materials out of the state during the required time is freeport goods. An application for this exemption must be filed with the appraisal district by April 30 each year. Copies of this application complete with instructions and supplemental forms are available on this site or obtained from the appraisal district.

Pollution Control Property

A person is entitled to an exemption from taxation of all or part of real and personal property that the person owns and that is used wholly or partly as a facility, device, or method for the control of air, water, or land pollution if it qualifies on January 1. A person seeking an exemption under this section shall provide the chief appraiser an exemption application on or before April 30 and a copy of the letter issued by the executive director of the Texas Commission on Environmental Quality under Subsection (d) determining that the facility, device, or method is used wholly or partly as pollution control property. A person seeking this exemption must render the pollution control property when filing a timely rendition.

Solar

Property owners may be eligible to claim exemptions on the installation or construction of solar and wind-powered energy devices that are primarily used to provide energy on-site.

In order to be eligible for this exemption, a property owner must own the property and system on January 1 of the year. Leased systems do not qualify for an exemption. However, leased systems are considered personal property and should not be taxed as part of your real property.

Property owners can submit an application along with supporting documents detailing the installation date and total output of the system in kilowatts. If the device was installed prior to the purchase of the home or was included as part of the purchase price, property owners should include a statement to that effect.

Completed applications must be filed no later than April 30 of the year for which a property owner is requesting an exemption.

If you lease your solar device, please inform the appraisal district by email at comalad@co.comal.tx.us and include the property address, CAD property ID number, and a statement that the system is leased.

Motor Vehicle Used for Production of Income and for Personal Activities

An individual is entitled to an exemption from taxation of one motor vehicle the individual owned on January 1. The exemption will only apply to a vehicle used during their occupation or profession and also used for personal activities that do not involve the production of income. This exemption does not apply to a motor vehicle used to transport passengers for hire (such as but not limited to, a taxi, bus, or limousine). You must file the application between January 1 and April 30. Attach a copy of the current vehicle registration receipt to the application. Failure to do so will result in the denial of the exemption. You may protest a denial of the exemption to the Appraisal Review Board. For the purposes of this application, an individual is one person or owner, as in a sole proprietor (not a partner, corporation, or cooperative). Motor vehicle means a passenger car or light truck. Passenger car means a motor vehicle, other than a motorcycle, golf cart, taxi, bus or limousine, designed or used primarily for the transportation of people. Light truck means a commercial motor vehicle that has a manufacturer’s rated carrying capacity of one ton or less.

Other Exemption Information

5-Year Homestead Exemption Audit Information

Appraisal districts are required to audit Homestead exemptions once every 5 years to confirm that the property owner still qualifies for the exemption.

You may view the approved policy for the Comal Appraisal District’s Homestead Audit program here.

Please do not file a new application unless we request you to do so.

Multiple Owners

Properties with multiple owners may be eligible for homestead exemptions under specific circumstances. Married couples are considered community property owners, with each spouse having 100 percent ownership. Heir property owners may also be eligible for homestead exemption.

In the case of partial ownership of uninherited property between non-married individuals, the amount of exemption is based on the percentage of ownership.

Selling or Buying a Home with an Existing Homestead Exemption

When you sell or buy a home, the taxes for the year will generally be prorated at the closing. This doesn’t actually change your tax liability; the tax assessor will calculate that later in the year. The proration at closing will be based on estimated taxes due. You should be aware of the rules regarding homestead exemptions so that you are prepared if your actual tax liability turns out to be different.

If you buy or sell a home that has only a general homestead exemption on it, the exemption normally stays in place for that entire tax year. The final taxes for the year will reflect the exemption. However, the new owner will have to qualify for the exemption by filing an application in his or her own name for the following year.

For example, if a property is appraised at $100,000 in the prior year, and sales information is received that causes the District to increase the value to $115,000 in the current year, the property will have a market value of $115,000, but the assessed value will be $110,000 ($100,000 X 110%). When a property with the limited appraised value sells, the limit is removed, and taxes will be based on the market value.

Below is an example of how taxes are affected when a property with general homestead and appraised value limitation sells:

| Current Owner w/ HS | New Owner w/HS | New Owner w/o HS | |

| Market Value | $100,000 | $100,000 | $100,000 |

| Assessed Value (limited appraised) | $ 90,000 | $100,000 | $100,000 |

| Taxes | $1,630.84 | $1,852.18 | $2,766.60 |

If the home you buy has had a cap in place for several years, be aware that the value of the home, and the taxes, may increase substantially in the year following the year you purchase it. This is because your cap won’t take effect until the second year after you purchase the home.

When a property sells with an over-65 or disability exemption, the effect on taxes can be dramatic. While the general homestead exemption remains with the property for the remaining portion of the year, property owners can transfer the over-65 or disability exemption to their new home, causing the taxes from the date of sale to be prorated at a higher amount. If the property owner does not transfer these exemptions, they will remain with the property until the next tax year. Since the taxes for the school districts and other entities are frozen at the amount that was assessed when the property owner qualified for the exemption, once these exemptions are removed, the tax freeze is also removed.

In the first quarter of each year, the Comal Appraisal District develops a list of all properties with a prior year homestead exemption which, during that same year, were sold to a new owner. Then, as required by law, the district cancels the old exemption as of January 1 of the new year and mails the new owner an exemption application form. However, you should act to protect your rights by ensuring that we have transferred ownership on the new home and that you have timely filed the homestead exemption application.

Homestead Cap Loss

An additional benefit of the general homestead exemption, especially in an appreciating housing market, is the homestead cap, or limitation on increases in appraised value. The cap applies to your homestead beginning in the second year you have a homestead exemption. The cap law provides that if you qualify, the value on which your taxes will be calculated (called your appraised value) cannot exceed the lesser of:

- This year’s market value; or

- Last year’s assessed value, plus 10% plus the value added by any new improvements made during the preceding year.

How to Complete the Homestead Exemption Application (Form 50-114)

- Fill out application completely.

Complete the top section.

- Appraisal district name (Comal)

- The year(s) you are applying for the exemption – you can apply back two years

- Appraisal District Account Number. This ID number can be found on our website using the property search feature and is listed as the Property ID Number.

Section 1: Exemption(s)

Complete Section 1 and select all exemptions that apply. Be sure to check General Residence Homestead Exemption in addition to Disabled Person, Person Age 65 or Older, or 100% Disabled Veteran.

Section 2: Property Owner/Applicant

Complete Section 2 and if a name does not match the ownership of record due to marriage, divorce, etc., please attach proof.

Section 3: Property Information

Complete Section 3 answering all questions completely.

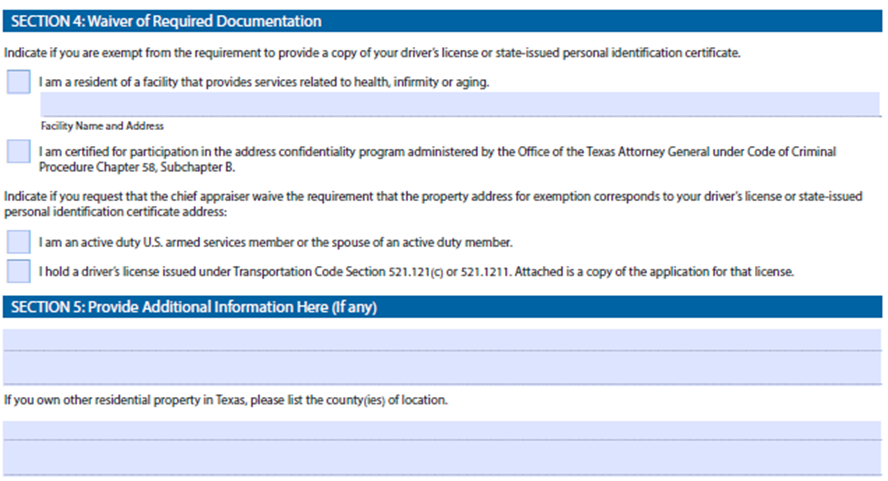

Section 4 and 5: Waiver of Required Documentation

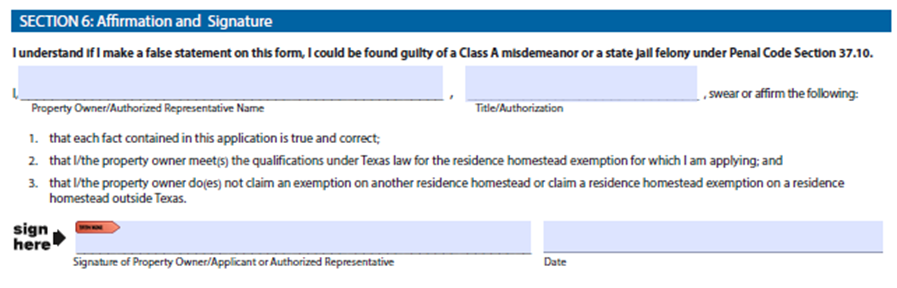

Section 6: Affirmation and Signature

Complete Section 6 including signing and dating the application. You are affirming that you have not claimed another residence.

It is a crime to make false statements on a homestead application or to file on more than one property. You could be found guilty of a Class A misdemeanor or a state jail felony under §37.10, Penal Code.

2. Submit the requested documentation.

Submit the requested documentation.

- For all applicants, attach a copy of your current TX driver’s license or TX ID card. You may be exempt from this requirement onlyif you reside in a facility that provides services for health, infirmity or aging (attach proof); or a certified participant of the Address Confidentiality Program (ACP) for victims of family violence, sexual assault or stalking (attach proof). The address listed on your TX driver’s license or TX ID card must match your homestead address. This requirement may be waived if you or your spouse or parent hold a driver’s license under §521.121 © or §521.1211 for a federal judge including a federal bankruptcy judge, a marshal of the U.S. Marshals’ Service, a U.S. Attorney or a state judge or peace officer (attach proof); or for active duty members of the U.S. armed services and spouse (attach proof).

- If married, both spouses must provide valid and current ID information or driver’s license.

- If you and your spouse do not have the same last name, please include a copy of the marriage certificate

- If there is more than one owner, and they are not married, each owner must provide valid and current ID information or driver’s license.

- If the ownership of the property is in the name of a trust please include pages…. from the trust document.

- For Disabled Person Exemption, attach proof of your disability including the date your disability began.

- For Age 55 or Older Surviving Spouse of individual who qualified for the Age 65 or Older Exemption or the Disabled Person exemption, attach spouse’s death certificate, list name of deceased spouse, and date of death on the application.

- For exemptions claimed on another property or on your previous residence, list the property address and if located outside of Comal County, attach documentation from the other appraisal district verifying removal of the exemption.

- For a residence less than 100% complete on January 1 of the year application is made, attach proof that of residency that proves you resided at your residence even though it was not 100% complete on January 1 (such as a utility bill dated on or before the date exemption is requested) that was mailed to you at the property address.

- For Cooperative Housing and you have an exclusive right to occupy the unit because you own stock in a cooperative housing corporation, attach a copy of the Certificate of Membership Purchase.

- For a resident of a facility that provides services for health, infirmity or aging, attach a letter from the facility stating the applicant’s date of residency and confirmation of services received relating to health, infirmity or aging.

- For a certified participant of the Address Confidentiality Program (ACP) for family violence, sexual assault, or stalking (Subchapter C, Chapter 56, Code of Criminal Procedure), attach proof of participation.

- For a holder of a driver’s license under §521.121 (c) or §521.1211 you or your spouse or parent hold a driver’s license under §521.121 © or §521.1211 for a federal judge including a federal bankruptcy judge, a marshal of the U.S. Marshals’ Service, a U.S. Attorney or a state judge or peace officer who have omitted the residence address in lieu of the courthouse/precinct address in which the license holder or spouse serves, attach a copy of the license application from TX Department of Transportation.

- For an active duty member of the U.S. armed services and spouse, attach a copy of your military ID card or that of your spouse AND a copy of a utility bill for the homestead property in your name or your spouse’s name and driver’s license.

- For Age 65 or Older, Heir Property, or Disabled Person who is not specifically identified on a deed or on the recorded instrument as an owner of the residence homestead, attach an affidavit (included with the application) or other compelling evidence establishing the applicant’s ownership of an interest in the homestead.

- For Manufactured Homes, attach a copy of the statement of ownership and location issued by the TX Department of Housing and Community Affairs AND a copy of the purchase contract or payment receipt showing you are the owner. If after making a good faith effort, you are unable to establish ownership as stated above, complete the sworn affidavit (included with the application).

Tax Ceiling Basics

TAX CEILINGS BASICS

If you have an over-65 or a disability homestead exemption you should be benefitting from a tax “ceiling” applied to your school taxes. If you decide to move, you can request a Tax Ceiling Certificate from your former appraisal district (or the same appraisal district if you move to a different home in that county) that may help reduce the school taxes on your new home.

It’s important to understand how this works. The tax ceiling is an “upper limit” dollar amount applied by your local school district’s tax office to your school taxes. It is set when you first qualify for either the over-65 exemption or the disability exemption. However, the legislation enabling the school tax ceiling for the disability exemption did not become effective until January 1, 2004. Before that date there was no school tax ceiling in place for disability exemptions, so the ceiling will usually have more effect on over-65 tax ceilings.

Generally, your school taxes can never go above the tax ceiling for as long as you live in your home. Taxes may be lower than the ceiling for some years, but never higher. The only exception would be if you significantly improved your house; for example, by adding a new room or a second story. (Normal repairs and maintenance such as a new roof or new paint do not count.) If significant improvements were ever made, then a new tax ceiling including the improved value would be calculated.

TAX CEILING CERTIFICATE BASICS

What happens if you move? First you need to apply for the over-65 exemption or the disability exemption on your new home. When you get the new exemption, you can benefit by transferring the percentage of school taxes paid on your former home. Please note: it is not the “upper limit” dollar amount but the percentage of school taxes paid that is transferable.

For example, if your school tax ceiling is currently $1,000, that number is compared to what you would be paying in school taxes without the tax ceiling in place. If you would be paying $4,000 in school taxes, then the percentage of taxes you are paying is 25%. (1,000 divided by 4,000 = 1/4 or 25%.) It is this percentage that is transferable by the Tax Ceiling Certificate. This means that if the school taxes in your new home would be $5,000 with your new over-65 or disability exemption in place, your new school taxes could have the 25% limit transferred and applied from your former home. Then your new school taxes would only be 25% of $5,000 or $1,250. That’s a savings of $3,750 per year, which can make a big difference if you are on a fixed income.

Frequently Asked Questions

Frequently Asked Questions

What is an exemption?

An exemption removes a portion of your property value from taxation.

Do I qualify for a Homestead Exemption?

If you own your home and it is your primary residence, which means you live in it most of the time, and you owned it as of January 1, you qualify for a General Homestead exemption. It cannot be an investment property or vacation home.

If you own your home, it is your primary residence and you are 65 years of age or older, you qualify for both a General Homestead and an additional exemption based on your age.

There are also special exemptions for disabled homeowners and disabled veterans and their survivors.

Homestead exemptions are not automatically applied when purchasing a home in Texas and are not available to corporations, partnerships or LLCs. A trust-owned property must meet specific criteria to be eligible.

How do I apply for an exemption?

You may visit the “Forms” tab and download the desired exemption application. You can also call the Appraisal District at (830) 625-8597 to request that a form be mailed or emailed to you. Once completed, and the required document(s) are attached, you can:

1) Mail to: 900 S. Seguin Avenue, New Braunfels, TX 78130,

2) Email in PDF format to: comalad@co.comal.tx.us

3) Drop off at the appraisal district building at: 900 S. Seguin Avenue, New Braunfels, TX 78130

Is there a deadline to apply?

You should file your residential homestead exemption application between January 1 and April 30. If your application is received by April 30, this allows the district time to process it before tax statements come out in the fall.

In Texas, you can file up to two years after the date the taxes would have become delinquent, or even later if you meet one of the following criteria:

- Disabled or 65+ years old: 2 years late

- Surviving spouse: 2 years late

- Disabled veteran: 5 years late

Is there a fee to file for an exemption?

There is no fee to file an exemption, and you do not have to hire anyone to file the exemption for you.

How long does it take for my exemption to be approved?

It currently takes about 90 days for applications to be processed and approved.

Can I apply for previous years?

Yes, you may apply for up to two years after the date taxes would have become delinquent. If you have already paid your taxes, you will receive a refund and then a new tax statement with a lower amount. This is available for Residence Homestead and 100% Disabled Veteran exemptions.

Do I need to reapply every year for my homestead exemption?

No, you do not have to reapply, unless the chief appraiser requests a new application in writing or you move to a new residence.

I received a “Disapproval” letter, what does that mean?

A “disapproval” letter means we cannot approve the exemption until we have received the requested documentation and the property owner is given 30 days to provide the missing documentation. A “denial” letter means that we did not receive the documentation needed and the exemption is denied. A property owner would need to submit a new application and the necessary documents.

Do I qualify for a General Homestead on a mobile home if I do not own the land?

Yes, you need to include a copy of your title to the mobile home or a verified copy of your purchase contract with the exemption form.

I own more than one home, can I get a homestead exemption on both?

No, you may only receive a homestead exemption on your primary residence.

I will soon be 65, when should I apply for the over 65 exemption?

You may apply at any time during the year you turn 65 years of age. You will receive the exemption for the full year.

Do I need to file an application when I turn 65 years old, or is it automatically added?

If we have the owner’s date of birth on file, we will automatically add the exemption to the account. If you are unsure if we have that information on file for you, please contact us at (830) 625-8597 option 1.

Do I qualify for a General Homestead exemption if I occupy/live in a section of my business?

Yes, if you occupy or utilize a portion of the business as your primary residence and are not claiming a General Homestead exemption anywhere else, you may qualify for a Homestead apportionment.

Does a non-profit organization automatically receive a property tax exemption?

No, often organizations mistakenly believe they are entitled to a property tax exemption, because they received a federal income tax exemption under Section 501(c)(3) of the Internal Revenue Code or an exemption from State sales taxes. The Constitutional requirements for property tax exemptions are different than the provisions covering income and sales taxes. A non-profit organization may qualify for a total exemption from property taxes, but they must apply by April 30th. Refer to the Forms page for exemption applications and requirements.

Do I have to receive disability benefits to qualify for the disability exemption?

You do not have to be receiving disability benefits, but you must meet the definition of disabled given above. If you receive disability benefits under the federal Old Age, Survivors, and Disability Insurance Program through the Social Security Administration, you will qualify. Disability benefits from any other program do not automatically qualify you for this exemption.